Who We Are

LGAI is powered by a team of professionals with deep experience across finance, law, data analysis, and public policy. We keep individual identities in the background because our credibility rests on the rigor of our research and the transparency of our methodology — not on personalities.

Our team shares a strong commitment to fiscal responsibility and nonpartisan analysis. We believe citizens deserve clear, accessible information about how their tax dollars are being managed, without unnecessary complexity or political spin.

We begin every project without political assumptions. Through investigation, the facts can lead us to clear conclusions about performance and accountability. While we never endorse candidates or engage in campaign activity, our findings can implicitly favor or oppose someone based on their record. We raise awareness so citizens can make informed decisions — we do not tell them how to vote.

We operate with a focus on America First principles and primary fiscal responsibility. Our work is driven by facts, not rhetoric.

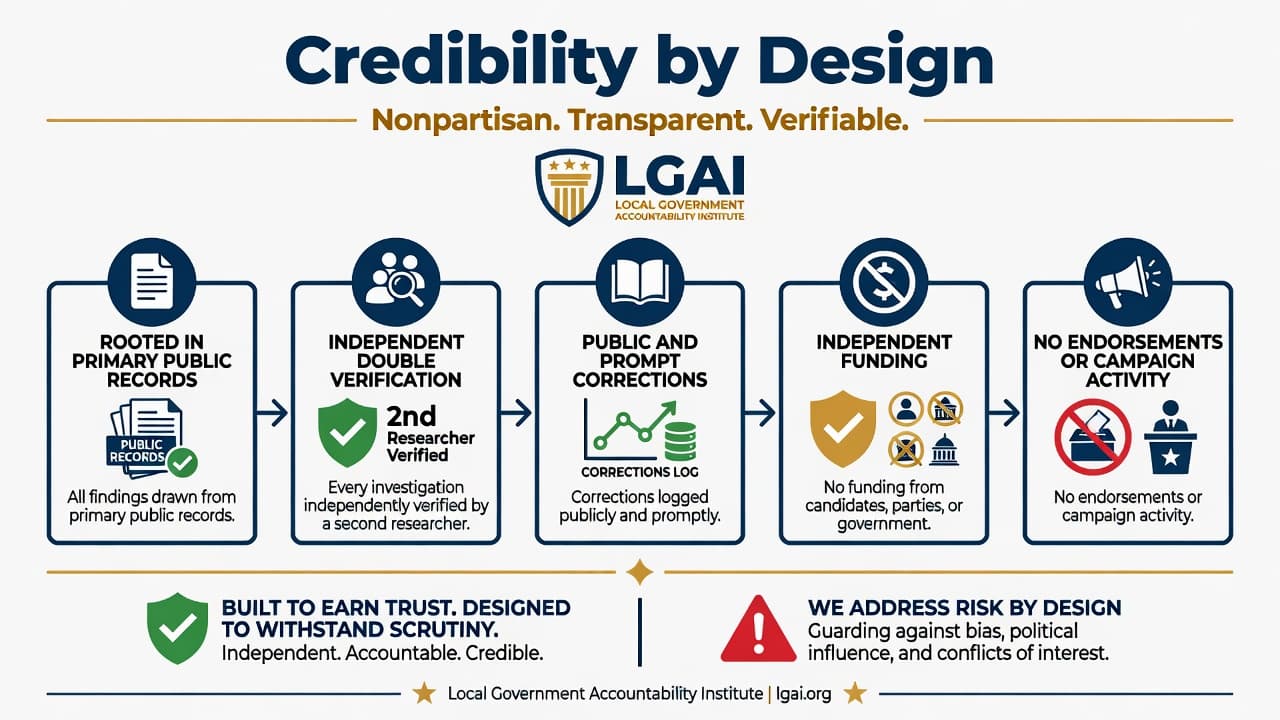

Why You Can Trust Our Work

LGAI operates with structural safeguards designed to maintain independence and accuracy:

Our credibility comes from method, not from claims of neutrality. We start every project without political assumptions and follow the evidence wherever it leads. When the record shows poor financial stewardship or conflicts of interest, we report it directly.

Our Approach

We begin every project without political assumptions. Our process combines deep document review with comparative benchmarking against similar jurisdictions and relevant economic data. When the records reveal patterns of poor financial stewardship or conflicts of interest, we report those findings directly.

We do not endorse candidates, engage in campaign activity, or accept funding from political parties or government entities. Our only objective is to deliver rigorous, fact-based research that supports public accountability.

How to Reach Us

Submit the contact form to send a tip, request a correction, ask a media question, or send general inquiries. Correspondence may also be sent via U.S. Mail to LGAI's Washington, D.C. office:

Local Government Accountability Inc

1250 Connecticut Avenue NW

Suite 700 PMB 5459

Washington, DC 20036

202-349-3720 (main)